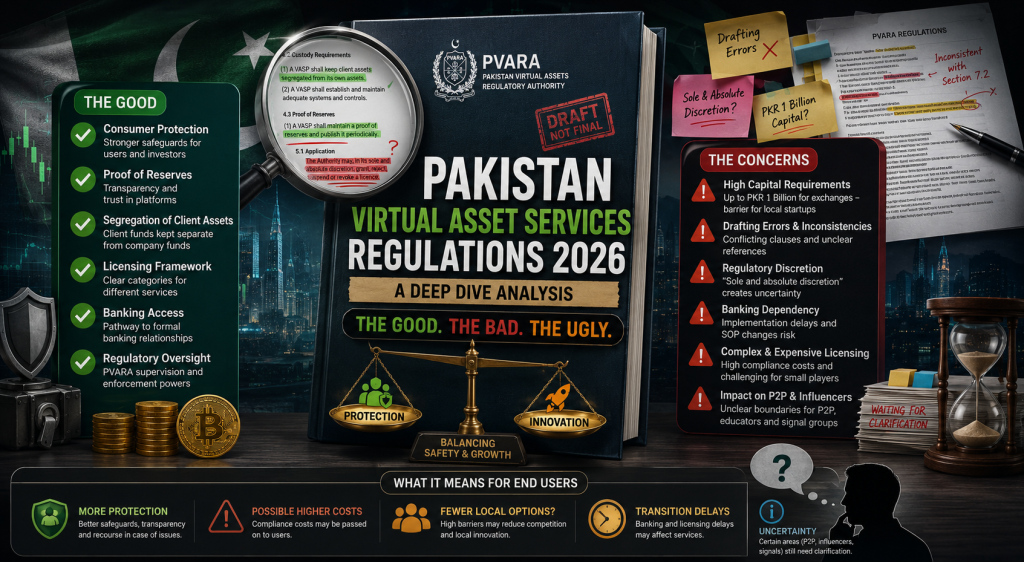

The Good, The Bad and the Ugly

Pakistan has fundamentally changed direction.

A few years ago:

• Banks avoided crypto.

• Regulators were hostile.

• Exchanges had no path to licensing.

Now:

• Parliament has passed the Virtual Assets Act 2026.

• PVARA exists as a dedicated regulator.

• SBP has opened a path for banking access to licensed VASPs.

• International exchanges are pursuing licenses.

The question is no longer “Will Pakistan regulate crypto?“

That question is already answered.

The real question is whether the final rules are balanced enough to encourage local Pakistani crypto businesses instead of only attracting large foreign players and how quickly safeguards are placed for the normal crypto consumer.

A Complete Regulation

The 2026 framework is much more mature than the 2025 NOC-style regime. It creates a serious licensing architecture for exchanges, brokers, custody, transfer/settlement, lending, derivatives, asset management, issuance, advisory, and mining-related services. The good news is that it strongly improves consumer protection, custody safety, disclosure, proof-of-reserves, cyber controls, complaints, market abuse controls, and segregation of client assets.

But the combined Regulations plus Handbooks are heavy and are mandatory to be read in conjunction. They look closer to a full financial-market regulatory system than a startup-friendly crypto framework. That is not automatically bad, but in Pakistan’s context it could become counterproductive if capital requirements, bank-dependency, licensing delays, vague discretion, and high compliance costs prevent local businesses from operating legally. These capital requirements may disproportionately favor well funded foreign firms over local startups.

The biggest policy fault is this: Pakistan may create a framework that is safe on paper but too expensive, slow, or uncertain for some Pakistani crypto businesses. If that happens, users will keep using offshore exchanges, informal P2P dealers, Telegram/WhatsApp groups, cash exchangers, VPNs, and unregulated stable coin channels.

Drafting Faults And Errors

The consultation period of 16 days(PVARA official X handle posted about this today) is far too short for a framework of this size. The Regulations are 77 pages and the Handbook(s) are 118 pages. These documents affect exchanges, banks, miners, traders, freelancers, influencers, tax authorities, law enforcement, startups, and ordinary citizens.

There are still placeholders and blanks: PKR [X], PKR [x], incomplete fee/date fields, and an orphan xxx. in the definitions.

There are drafting/typing issues such as inPakistan, Authoirty, without immediately, risk profile;;, carryon, guidance. guidelines, this Regulations, promotors, and he integrity.

There are numbering and cross-reference problems, including skipped/missing numbering and some clauses that appear pasted from different drafting styles.

Record retention is inconsistent. The Regulations mention seven years in multiple places, while the Handbook says activity-handbook records are at least five years unless a longer period applies. If AML/CFT records are longer under separate laws, the documents should say so cleanly.

The Regulations say some guidance-style material should not create independent legal obligations, but the Handbooks often use mandatory language like “shall” and attach enforcement consequences. That creates confusion over whether a Handbook is guidance, binding secondary law, or licence-condition material.

The phrase “sole and absolute discretion” appears in relation to margin trading powers. That is too broad. A regulator may need emergency powers, but they should be reasoned, proportionate, time-bound, and reviewable.

“Public interest” and “national interest” style powers should be tightened. Otherwise they can become unpredictable tools for suspension/cancellation.

Counterproductive Risks For Pakistan

Minimum paid-up capital is very high: PKR 1 billion for exchanges and token issuers, PKR 500 million for lending/derivatives, PKR 200 million for custody/transfer/asset management, and PKR 25 million even for advisory. This may exclude local startups and favour banks, large conglomerates and foreign exchanges.

The Handbooks add even more cost: best execution, suitability, market surveillance, wallet-provider checks, custody assurance, half-yearly custody reports, whitepapers, operational resilience, detailed disclosures, and specialized policies for each activity.

Bank dependency is a major practical risk. Client money must generally be held with SBP-licensed banks. If banks hesitate to support VASPs, legal on-ramp/off-ramp channels will fail in practice as banks may take significant time to update internal compliance procedures, creating delays between regulatory approval and practical implementation

Insurance requirements may be hard to satisfy locally without providing an incentive to such insurance providers to be in the forefront. Pakistani insurers may not yet offer meaningful crypto custody, cyber, crime, and key-management coverage.

The framework may unintentionally push smaller traders and businesses into informal channels as licensing is too expensive or ends up to be very slow.

Retail protection is improved, but high-risk activities like leverage, derivatives, lending, borrowing, staking/yield, and rehypothecation still need clearer retail restrictions, suitability tests, caps, or outright retail bans.

The professional-client opt-up remains risky unless thresholds and safeguards are made clear. Retail users should not be easily pushed into “professional” status to lose protections. The opt-up idea is not bad, but it can be abused unless the rules stop ordinary people from being pushed into a “professional” label they do not truly understand.

Special Sovereign Clients. The special treatment of “Sovereign Clients” and yield-related activity involving public-sector assets needs stronger guardrails. Public assets should not be exposed to crypto yield strategies without very high transparency and accountability. The concern is that if public-sector assets are put into these strategies, the losses are not just private investor losses. They could affect public money, state-controlled assets, or assets held on behalf of citizens. The Handbook does add some restrictions, for example it says Sovereign Client assets should not be put into unsecured lending, unrestricted rehypothecation, or structures that damage custody control/transparency/recoverability unless expressly approved.

In simple terms: the framework seems to allow the possibility of government/public-sector crypto assets earning yield. That may be useful in controlled cases, but it is dangerous if done quietly or loosely. Public assets should not be used in risky crypto yield strategies without strong transparency, oversight, and accountability.

Positive Aspects of PVAS Regulations 2026

Self-custody software/hardware is not treated as custody if the customer keeps exclusive control. General education, research, and non-personalized market commentary are not automatically advisory services.

Exchanges may list virtual assets without prior product approval if conditions are met. This is positive and avoids making PVARA approve every token one by one.

Client assets must be segregated and cannot be treated as the VASP’s own property. Custodians must maintain proof-of-reserves/independent validation and strong key-management controls. Client assets cannot be used, pledged, lent, staked, or rehypothecated merely because the VASP has a licence. Explicit informed consent is required.

Complaint handling, public disclosures, client agreements, risk warnings, dispute pathways, and monthly statements for retail users are good consumer protections.

Pure mining is not itself treated as a VASP service unless the mining business involves client assets, client money, pooling, reward distribution, or services to third parties.

P2P Trading, On-Ramp And Off-Ramp

Pakistani citizens are still facing Bank chain disputes and FIA/NCCIA related issues, while PVARA has opened a grievance/complaint cell to address such cases but without any public disclosure of how many cases received vs solved, we do not know the efficacy of such arrangements and have to rely on such draft documents to assess how things will develop in Pakistan.

The documents do not appear to impose a clean blanket ban on P2P trading. They also do not clearly say, “P2P is freely allowed.” The result is mixed. For ordinary individuals occasionally buying/selling their own crypto, the key phrase is “by way of business.” If someone is just personally trading, that likely should not be a VASP activity.

But if someone operates as a P2P merchant, exchanger, OTC desk, or repeatedly buys/sells crypto to the public for spread/profit, that likely falls into licensing territory.

Possible categories:

- A P2P merchant buying/selling from users as a business may fall under Broker-Dealer Services, because the person is dealing in virtual assets as principal or agent.

- A platform that matches buyers and sellers may fall under Exchange Services.

- A service that moves crypto between wallets or completes transfer/settlement for customers may fall under Transfer and Settlement Services.

- If the merchant holds customer fiat or crypto during the transaction, Custody or client-asset rules may also apply.

- If it provides PKR payment rails, that strengthens Pakistan nexus and regulatory scope.

For on-ramp/off-ramp, the framework seems to prefer regulated channels. Client money held by a VASP must generally be kept in segregated client accounts with SBP-licensed banks. So formal on-ramp/off-ramp is expected to run through licensed VASPs and banking/payment channels which might be beneficial for Pakistan. Informal P2P cash/bank-transfer merchants may be treated as unlicensed VASP activity if done as a business.

Influencers, Trading Signals And Communities

General free education, market commentary, factual information, research, or non-personalized opinions are not automatically Advisory Services.

So a public post like “Bitcoin looks weak today” or “Here is how support/resistance works” is likely not a licence activity by itself.

But if an influencer says, professionally or commercially, “Buy XYZ now,” “Sell this coin,” “Enter this trade setup,” or gives recommendations presented as suitable for a person or group, especially with a paid community, that can move toward Advisory Services.

Separate treatment based on category of influencer

Free influencer/community:

- General education or non-personalized commentary: probably no VASP licence.

- Repeated buy/sell calls, signals, or targeted recommendations: possible Advisory Services risk, depending on whether it is professional, personalized, or commercial.

- Paid promotion of a token/exchange without disclosure: not necessarily a separate VASP category, but may breach marketing, disclosure, conflict, or market-abuse rules if connected to a licensed entity or issuer.

Paid trading community:

- Paid signals, trade setups, entry/exit levels, or “buy/sell this coin” calls are much more likely to be treated as Advisory Services.

- If the operator manages funds, copies trades, controls accounts, or makes decisions for users, it may become Management and Investment Services.

- If the operator routes orders or executes trades for users, it may become Broker-Dealer Services.

- If it pools money/assets, custody and asset-management issues may arise.

Free educational crypto content is mostly safe, but paid signal groups and professional “trade call” communities are exactly the sort of thing PVARA may treat as regulated advisory activity, especially if Pakistani users are targeted.

VASP Licence Type and Fee

| # | Licence category | What it broadly covers | Minimum paid-up capital |

|---|---|---|---|

| 1 | Advisory Services | Professional/personalised VA recommendations | PKR 25,000,000 |

| 2 | Broker-Dealer Services | Dealing as principal/agent, arranging buys/sells, order facilitation | PKR 100,000,000 |

| 3 | Custody Services | Safeguarding client crypto/fiat/private keys | PKR 200,000,000 |

| 4 | Exchange Services | Exchange, order book, matching system, swap/trading venue | PKR 1,000,000,000 |

| 5 | Lending and Borrowing Services | VA lending, borrowing, credit, margin/financing arrangements | PKR 500,000,000 |

| 6 | Virtual Asset Derivatives Services | Derivatives, margin, leverage products | PKR 500,000,000 |

| 7 | Virtual Asset Management and Investment Services | Portfolio/discretionary management, staking as part of mandate | PKR 200,000,000 |

| 8 | Virtual Asset Transfer and Settlement Services | VA transfers/settlement between wallets/parties/payment rails | PKR 200,000,000 |

| 9 | Fiat-Referenced Token Issuance Services | Issuing/administering fiat-referenced tokens/stablecoins | PKR 1,000,000,000 |

| 10 | Asset-Referenced Token Issuance Services | Issuing/administering asset-referenced tokens | PKR 1,000,000,000 |

| 11 | Mining-related VA Activities Licence | Mining services involving third-party/client assets or funds | Not listed in Schedule-I capital table |

Important: the Regulations mention “Mining-related virtual asset activities Licence,” but the Schedule-I capital table does not give a separate minimum paid-up capital for it. Pure self-mining by itself is not treated as requiring a VASP licence.

NOC Application Flow

| Fee type | Status in 2026 draft | NOC 2025 |

|---|---|---|

| NOC / preliminary approval processing fee | Required, but amount is blank: PKR [x] | No amount mentioned |

| Licence application processing fee | Required, non-refundable, but amount not provided | Not mentioned |

| Licensing fee | Required, but amount not provided | Not mentioned |

| Annual supervisory fee | Required, payable in advance, but amount not provided | Not mentioned |

| Renewal fee | Required where applicable, but amount not provided | Not mentioned |

| Other charges | May be required as published in Rules, but amount not provided | Not mentioned |

NOC / Licence Timeline

| Stage | Step | Timeline / deadline |

|---|---|---|

| 1 | Applicant prepares NOC application using Form-I/Annexure | No fixed preparation period |

| 2 | Submit NOC/preliminary approval application with required information and processing fee | Applicant-controlled |

| 3 | PVARA reviews whether NOC application is complete | No fixed time for “completeness” confirmation stated |

| 4 | PVARA grants or refuses NOC after complete application | Within 60 days of receiving complete application |

| 5 | If NOC granted, applicant incorporates in Pakistan / proceeds with licensing readiness | NOC validity period applies |

| 6 | NOC validity | 3 months from issuance |

| 7 | NOC extension | One extension up to 3 more months, if applied before expiry and reasons recorded |

| 8 | Applicant applies for full VASP licence within NOC validity | Must be within valid NOC period |

| 9 | PVARA checks full licence application completeness | Clock starts only once PVARA confirms complete application |

| 10 | PVARA decides full licence application | Within 90 days of complete application |

| 11 | PVARA may extend licence decision period | Up to 60 additional days for complex/novel/consultation cases |

| 12 | PVARA grants licence, refuses licence, or grants limited-scope licence | Written reasons required for refusal / adverse condition |

| 13 | After licence grant, licensee must commence business within period stated in licence | Period not fixed in draft; stated in licence |

Note: If PVARA asks for more information, the full licence decision clock is suspended until the applicant provides it. That can make the real timeline longer than the headline numbers.

Good Changes From 2025 NOC

The 2025 regime was mainly a NOC/local incorporation/goAML gateway. The 2026 framework is a full licensing regime.

The new framework clearly separates activity types: advisory, broker-dealer, custody, exchange, transfer/settlement, lending, derivatives/leverage, management/investment, issuance, and mining-related services. Custody, segregation, proof-of-reserves, cyber controls, AML/CFT, complaints, public disclosures, and market abuse rules are much stronger.

The Handbooks clarify that general education and non-personalized research are not advisory services and further clarifies that exchanges can list assets without prior product approval, subject to internal due diligence and regulatory notification. The new rules provide transitional arrangements for existing operators.

Bad Changes From 2025 NOC

The framework is much more expensive and complicated. The 2025 NOC path was narrower but easier to understand. The 2026 framework creates multiple overlapping licences and Handbooks.

The capital thresholds are very high. The process can become slow: NOC, incorporation, full licence application, completeness checks, possible information requests, and possible extensions.

There is too much discretionary language left to PVARA. The combined Regulations plus Handbooks may be difficult for small Pakistani crypto businesses to comply with without lawyers, compliance officers, auditors, cyber consultants, and capital backing, As earlier mentioned it would imply that PVARA is currently considering international onboarding which if reasoned in depth and proved beneficial may be a different story.

Conclusion

Any update / progress towards regulations is a step in the right direction, but as a consumer – I just like many other are eagerly waiting for end user regulatory framework. The current approach of PVARA is to first regulate the industry players and later bring in regulatory / taxation framework for the consumer. While a dual sided approach may speed up the process if both the aspects were worked upon as that will allow the consumers to get over the everyday hassles of bank chain disputes and the confusion when we are asked to explain to a bank about a crypto-to-fiat offramp through existing channels. The biggest questions remain to be answered :

- Consumer taxation framework.

- Treatment of individual traders.

- Treatment of P2P users.

- Banking protection for legitimate crypto users.

- How quickly licenses will actually be issued.

- Which global exchanges will obtain licenses.

Editorial Note: Please let me know if any omission / invalid reference has been found, so that it may be fixed. The article has been written while consulting the PVAS Regulations 2026 and the various handbooks uploaded on PVARA official portal and minimum references have been made out of this context while a special mention / link has been created to understand the future aspect of P2P and Influencers operating in Pakistan out necessity.